The investing landscape has been anything but easy for investors to kick off 2026. In the first quarter, investors had to navigate a war with Iran, surging energy prices, private credit fears, and hawkish central bank rhetoric. Volatility as measured by the VIX Index jumped to the highest level seen since Liberation Day (April 2025). Global equities as measured by the MSCI AC World Index posted their worst quarterly return since 3Q22. And many equity indices dipped into correction territory, dropping more than 10% (e.g., NASDAQ, Dow Jones Industrial Average, German DAX, France CAC 40).

In addition, bonds failed to act as a safe haven as the Bloomberg Aggregate Index declined for the first time in five quarters. And the 10-year Treasury yield rose to a seven-month high. Commodities were the only bright spot, but it was driven by supply fears due to the war with Iran, which sent crude oil prices to the highest level in four years.

LISTEN NOW: Alternate View Podcast

While the economy slowed considerably at the end of 2025 (+0.5% QoQ GDP), there were positive signs developing to kick off 2026. Manufacturing finally exited a recession and homebuyers started emerging. Consumers remained resilient and the AI investment continued. As we move into 2Q26, tensions in the Middle East have added near-term uncertainty that could pressure economic growth. However, we remain optimistic that the conflict will not drag on for an extended period of time. We’re optimistic growth will end up positive for the year. In this quarterly commentary, we outline our base case for the economy and asset classes as uncertainty remains elevated.

Economy – Short-term pain likely; long-term still intact

Leading up to the conflict with Iran, the U.S. economy was on relatively stable ground. The ISM Manufacturing Index had entered expansion territory (a level above 50) for the first time in 11 months. Also, the service sector was strengthening, consumers started spending on more than just necessities, and core durable goods orders were on the rise. Even the housing market was showing signs of life as mortgage rates dipped to a four-year low and homebuilder sentiment was improving.

Conflict Extends Uncertainy

As the conflict with Iran has extended beyond the White House’s initial expectations (4-5 weeks) and more extensions to the ceasefire are likely, the economic outlook has become increasingly uncertain. Inflationary pressures, supply chain disruptions, and rising consumer costs are increasing the risk of a near-term economic slowdown. The surge in energy prices is not only an unforeseen tax on the consumer, but it is also reducing the benefit of the larger tax refunds we expected from the One Big Beautiful Tax Bill.

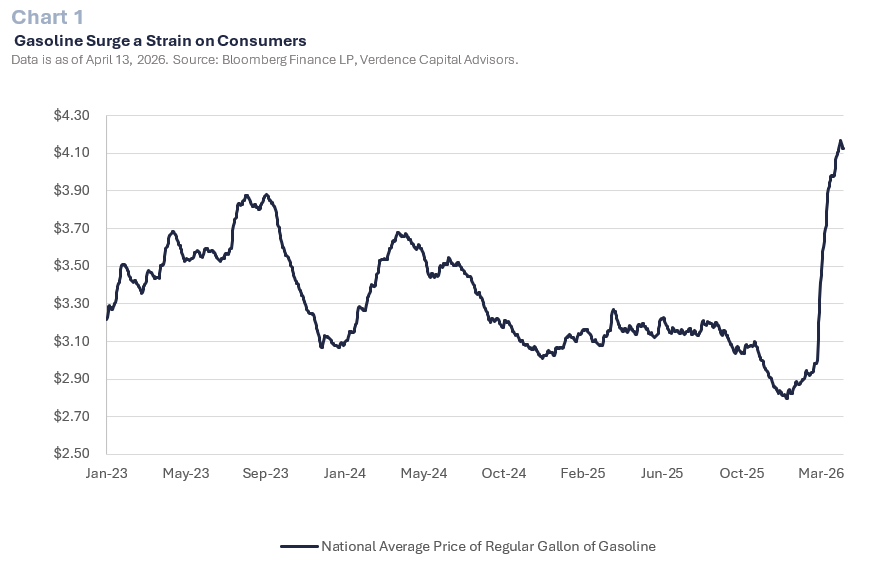

Higher Gas Prices Pressure Consumers

It is a general rule of thumb that for every $0.01 increase in the price of gasoline, it can reduce the annual spending power of the consumer by $1 billion.1 Therefore, the recent increase of over $1.30 per gallon of regular gasoline has the power to reduce $130 billion of annual spending power for consumers. (Chart 1). This exceeds the Tax Foundation’s estimate that up to $100 billion in additional refunds could be distributed this tax filing season.2

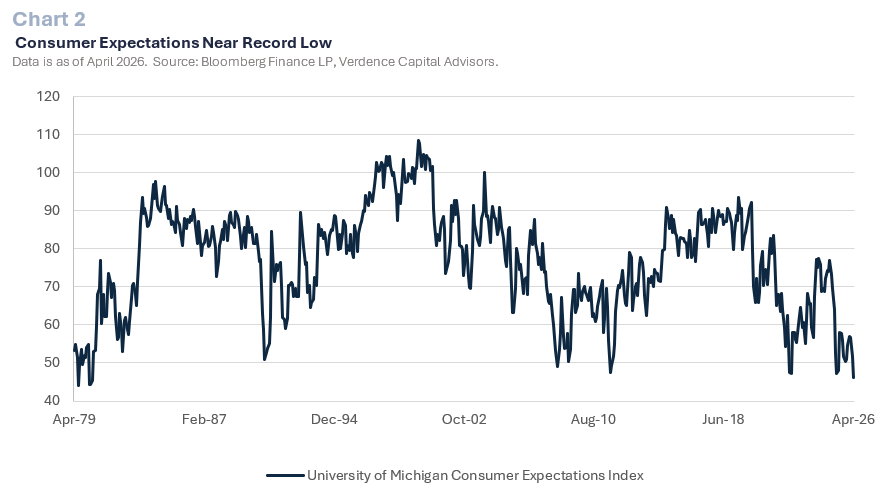

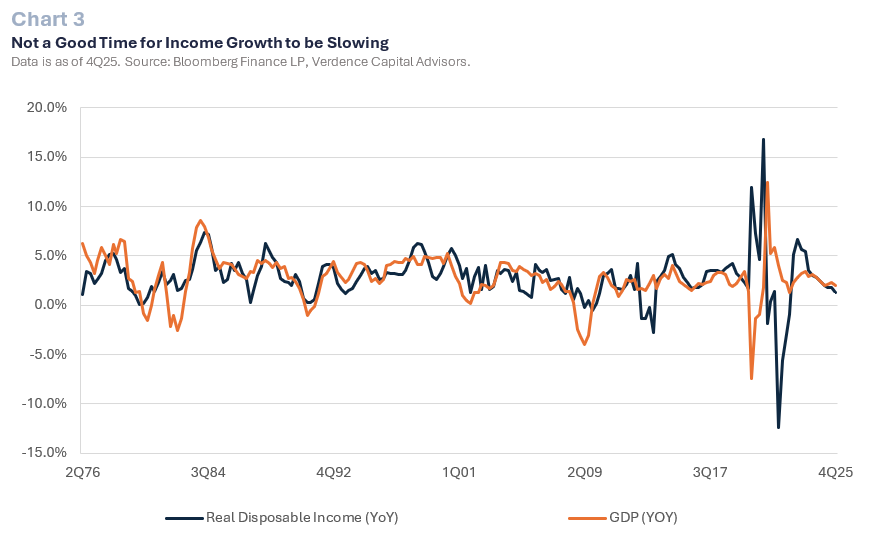

Consumer Confidence and Income Growth Weaken

In addition, this is coinciding with signs that the consumer is turning extremely pessimistic about the outlook for the economy (Chart 2). Plus the growth in real personal disposable income is steadily decelerating. Historically, there has been a relatively strong correlation between the growth in real disposable income and GDP. (Chart 3).

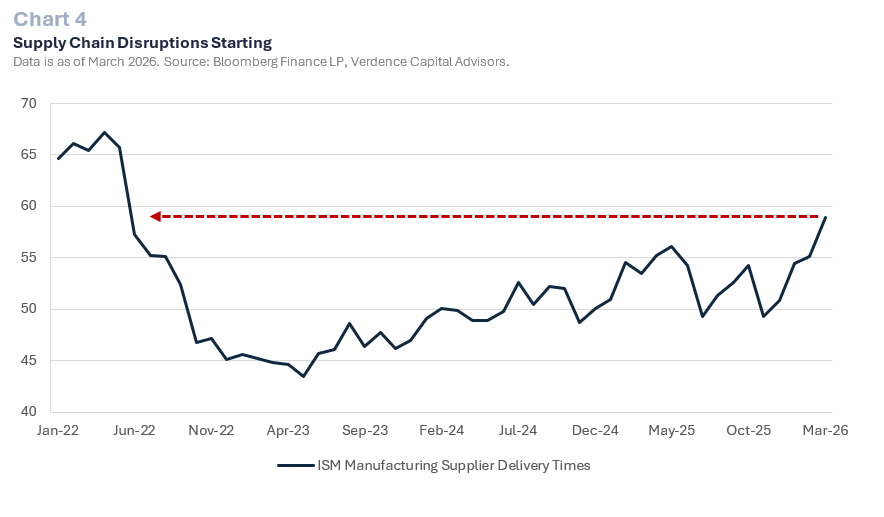

Business Sentiment and Supply Chains Under Pressure

The economic uncertainty is also evident in business sentiment. This is as businesses are now contending with rising input costs and supply chain disruptions. Small business optimism is at the lowest level since Liberation Day (April 2025). Business owners have reported the most pessimistic outlook on the economy since 2024. In addition, with the Strait of Hormuz not functioning normally, wait times for manufacturers receiving input materials rivals that seen in the aftermath of the pandemic. (Chart 4).

The Strait of Hormuz not only carries one fifth of the global oil supply and a quarter of the world’s natural gas. However, it also carries critical chemicals, fertilizer components, and helium that travel through the Strait. These are important for the production of everything from electronics to clothing, to medical equipment, semiconductor chips, and appliances.

Inflation Was Already Rising

As we discuss inflation, it is important to realize that even before the war began, inflation was creeping higher as tariffs started working their way through the economy. As of February, the Fed’s preferred inflation indicator (PCE Core) had been rising on a month-over-month basis and stuck at a 3.0% annual growth rate, which is well above the Fed’s 2% target. (Chart 5).

The ultimate impact of the war and subsequent increase in prices is still highly dependent on how long the conflict goes on and when the Strait of Hormuz can function normally again. Even if the conflict were to completely end tomorrow and shipping fully resumes in the Strait, it will take time to clear bottlenecks. In addition, some energy producers halted production due to a lack of storage so it will take time to operate at normal capacity again. As a result, we see upward pressure on inflation in the coming months.

Federal Reserve Shifts From Employment to Inflation

In recent meetings, the Federal Reserve has rightfully shifted their focus from weakness in the labor market to the upside risk in inflation. While the labor market has painted a mixed picture in 1Q26, temporary distortions from labor strikes and weather impacted the data. While hiring and job openings are moderating, labor demand is cooling as well, suggesting the labor market is moving closer to being in balance.

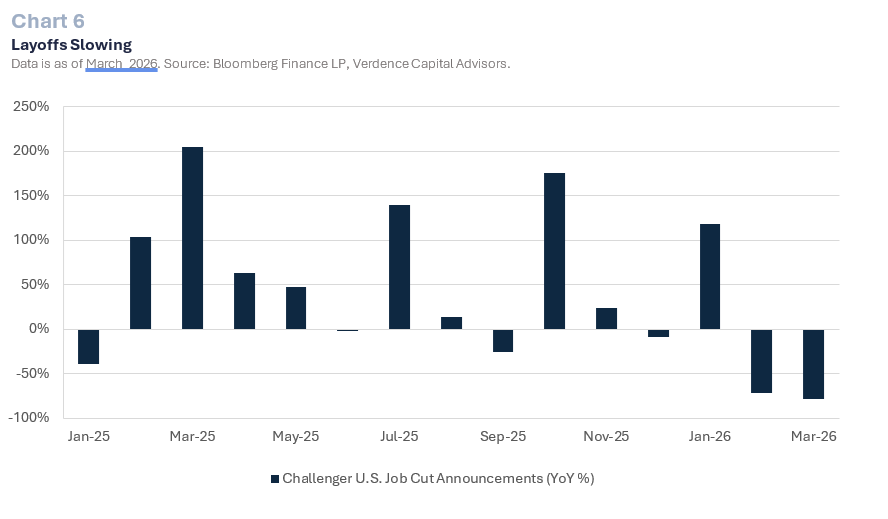

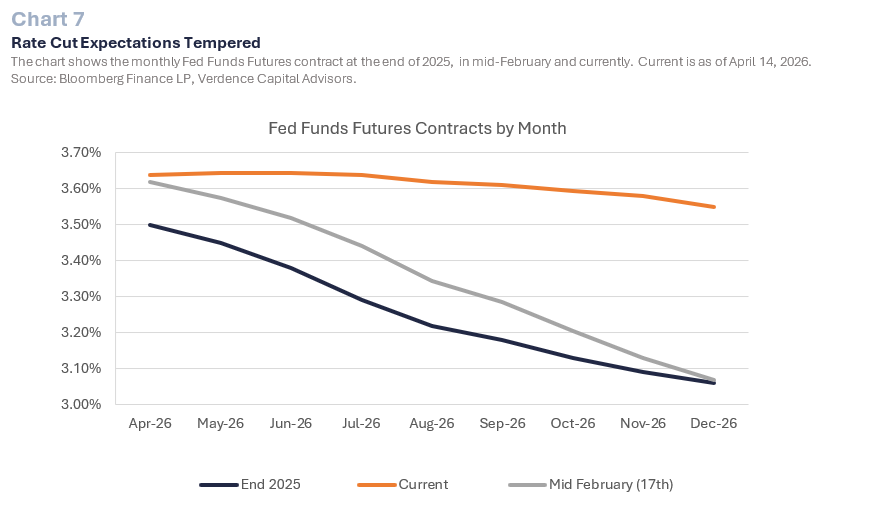

In addition, the unemployment rate is low by historical standards, and layoffs are slowing. (Chart 6). As a result, given increasing inflationary pressures and a labor market that has slowed but not collapsed is likely to keep the Fed on hold for 2026. Even before the war, the expectation for rate cuts in 2026 was being tempered compared to the end of 2025. (Chart 7).

Many Fed officials have been vocal about their concern over inflation and even the likely new Fed Chairman Kevin Warsh recently expressed concern that inflation can remain elevated.3 Although there is a view that the Fed may need to raise rates, at this point, that is not our base case scenario because we do not expect the war to be a prolonged event. Our view may change if tensions accelerate, oil prices hold above $100 bbl, and supply chain disruptions persist.

LISTEN NOW: Markets With Megan Podcast

Federal Reserve Bottom Line:

We believe the negative impact from the war with Iran (e.g., inflation, supply chain disruptions) will be contained mostly to 1H26. However, we also acknowledge the situation remains very fluid and we are constantly monitoring the incoming economic data to see if it will have a longer-lasting impact. The biggest threat is to inflation and its negative impact on the consumer, which is likely to result in subdued economic growth in 1H26.

Many of the positive fundamentals that had the economy gaining momentum before the war remain intact. AI spending continues, and while the labor market has softened, it remains strong by historical standards, and productivity is robust. The One Big Beautiful Tax Bill offers benefits beyond the tax refunds that are being eroded by higher gasoline prices (e.g., no tax on tips/overtime, bonus depreciation, expensing of R&D). In addition, the White House is fully aware that more than half the population does not approve of the war with Iran and midterm elections are right around the corner.

The unemployment rate is low by historical standards, and layoffs are slowing

Global Equities – Still waiting for a valuation repricing

Markets Whipsawed by Headlines

Investors were whipsawed in 1Q26 with the VIX Index (Volatility Index) temporarily spiking to levels not seen since Liberation Day (April 2025) and many major Indices falling into correction territory (a drop of 10% or more). However, as quickly as equities fell, it was common to see a similar rebound the following day or even intraday, depending on the news. The ever-changing headlines had investors and equity analysts scrambling to make sense of the long-term ramifications.

Valuations Remained Elevated

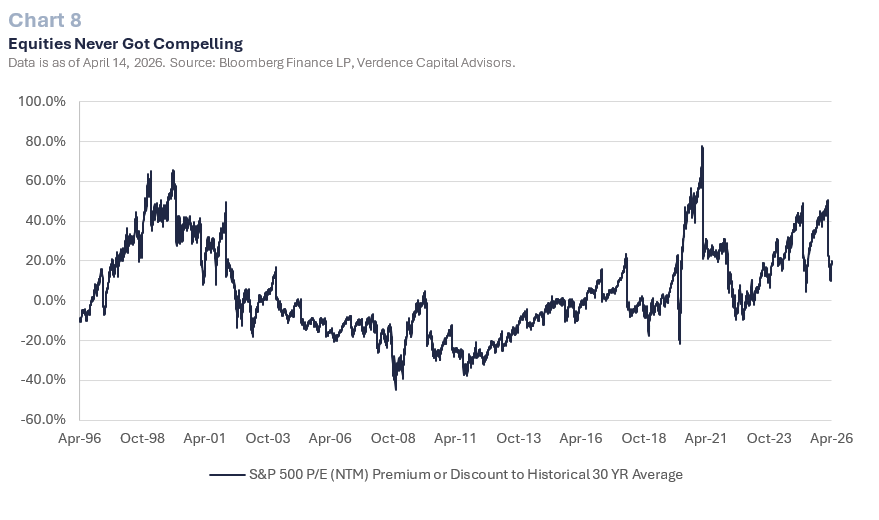

Despite the volatility and disappointing performance, global equities entered the conflict at significantly elevated valuations. As a result, even with some indices dropping more than 10%, valuations did not become sufficiently attractive to warrant aggressive buying in such an uncertain environment. For example, the forward price-to-earnings multiple of the S&P 500 never traded at a discount during the volatility. (Chart 8).

Selective Opportunities, But No Capitulation

That does not mean that specific stocks and sectors did not offer opportunities; that is why choosing active managers over passive managers is so important in the current environment. We also did not see many signs of capitulation, which would suggest the markets had fully priced in the looming risks. The VIX only briefly jumped above 30 (levels above 40 suggest capitulation), the percentage of stocks trading above their 50-day moving average remained elevated, and the put to call ratio never substantially increased.

Earnings Expectations Have Yet to Adjust

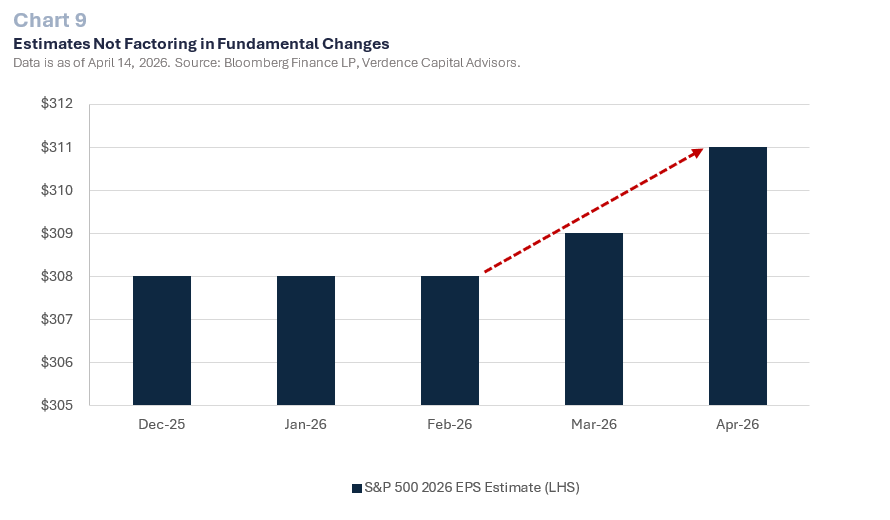

The other concern we have at this time is that we have not seen an adjustment to earnings for 2026. While our base case is the war will be a 1H26 phenomenon, we should see some repricing of earnings expectations now that inflation is a bigger risk than when we entered the year.

In addition, it is nearly 100% priced in the futures market that the Fed will not be cutting interest rates this year. This was not the case at the start of the year when at least two rate cuts and lower inflation were factored into earnings estimates. Instead, we have seen earnings estimates for 2026 increase since the conflict broke out. (Chart 9).

Near-Term Risks, Long-Term Opportunities

We believe there could be additional downside in the near term as investors reprice the aforementioned risks and the impact from the war starts showing up in economic data. We will continue to prioritize valuations, fundamentals and technical analysis over the political backdrop, as the path of the conflict remains unclear. From a valuation and fundamental perspective, we still favor small and mid cap stocks for the long run. Especially large cap equities which are still trading at a steep premium. Small and mid cap equities are trading at a discount and should benefit from a resumption of growth in 2H26. Investors may experience volatility around interest rates given small and midcap stocks can be interest rate sensitive but valuations are relatively cheap.

Global Diversification Still Matters

We also strongly recommend a well diversified approach, globally but with a focus on the developed international markets. We realize the developed international markets are not as cheap as they once were but if you do not have exposure we believe they are cheap compared to U.S. equities and have plenty of room to catch up, especially in a deglobalization environment.

Global Equities Bottom Line:

For equity investors, the start to 2026 was confusing and at times unsettling. The current geopolitical climate is already disconcerting, and the addition of regular 2-3% daily swings in equity prices throughout the quarter has only heightened investor concern. We expect volatility to continue in the near term, and history tells us that midterm election years also bring with them odds for a market pullback (average pullback of 18%).4 However, what history has also told us is that during geopolitical events and in midterm election years, the weakness often presents good long term buying opportunities. We will continue to monitor fundamentals and valuations and make adjustments to the portfolios when prices factor in the risks in 2026.

Fixed income – Not the traditional safe haven

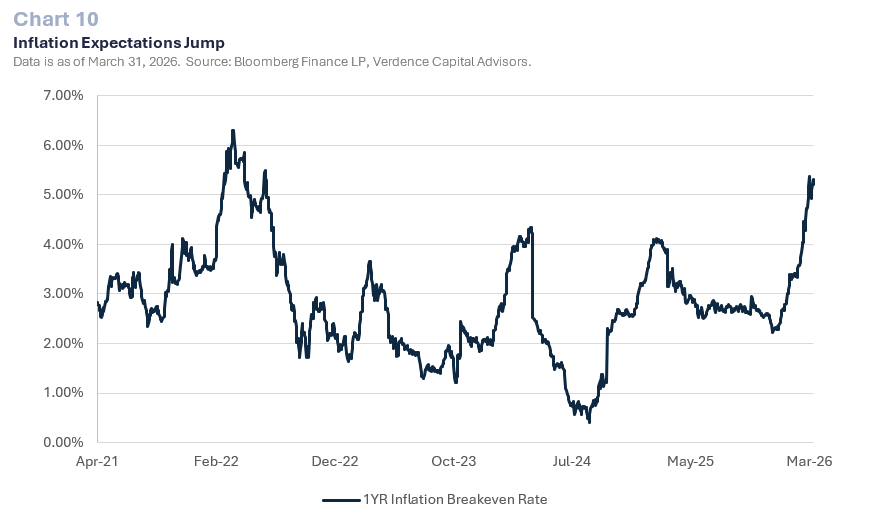

Bonds failed to offer the traditional safe haven for investors in 1Q26 as the Bloomberg Aggregate Index posted its first quarterly decline in five quarters. Yields rose alongside inflation expectations as oil prices jumped. Short-term inflation expectations rose to the highest level seen since 2022. (Chart 10). Private credit concerns hampered the performance of many sectors within the corporate space. Leverage loans and high-yield bonds posted their first quarterly decline since 2022. Short-term bonds outperformed long-term bonds, especially floating-rate bonds that benefited from the phasing out of rate cut expectations.

We recommend having a fixed income as a portfolio diversifier, but are cautious about the space in 2026 and beyond. We recommend taking a short to intermediate maturity stance across taxable and tax-free bonds. With inflation a looming risk in 1H26, there is likely additional upside in yields.

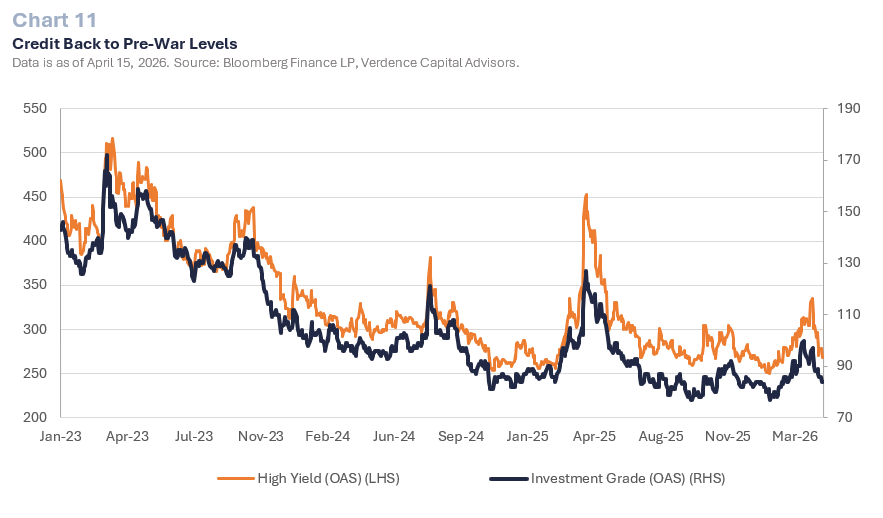

In addition, we have started to see mixed results from Treasury auctions as the participation rate of international buyers is declining. This is partially due to the rise in global yields which has allowed international buyers to purchase bonds in their own country without having to take on currency risk of purchasing U.S. Treasuries. We also remain cautious on credit. Even in the depth of the risk off sentiment in 1Q26, the extra yield investors demand to own high yield and investment grade debt (i.e., spreads) barely moved higher. In fact, currently, those spreads are back to pre-war levels. (Chart 11).

Fixed Income Bottom Line

Interest rates are likely to remain volatile, especially long-term rates, as we navigate through the inflation impact of the war with Iran. The moves in the near term are likely to be closely correlated to the price of oil. As a result, investors should remain defensive with credit and interest rate exposure, focusing on high-quality bonds with short or intermediate maturities. On a long term basis, we still remain cautious about long term bonds because we expect growth to accelerate in 2H26 and the burgeoning deficit is raising international concerns.

Alternatives – Uncorrelated assets in times of uncertainty

For qualified investors, alternative investments can perform well in the current uncertain economic and inflationary climate. For qualified clients who invest in private investments, they are spared the daily volatility seen in public markets and historically have been offered an uncorrelated asset. We believe that one of the more attractive long-term areas of alternatives is in the real asset space (both public and private).

Real assets can not only perform well in periods of stubborn inflation but also in periods of infrastructure investment. The infrastructure investment that is occurring due to artificial intelligence (e.g., electricity) and the potential for price appreciation and income should benefit investments in the real asset space, but diversification and active management is important in a period of slowing economic growth. We are avoiding any additional exposure to private credit but believe in the sector for the long run. Given the current uncertainty and lower quality private credit, due diligence is crucial at this time.

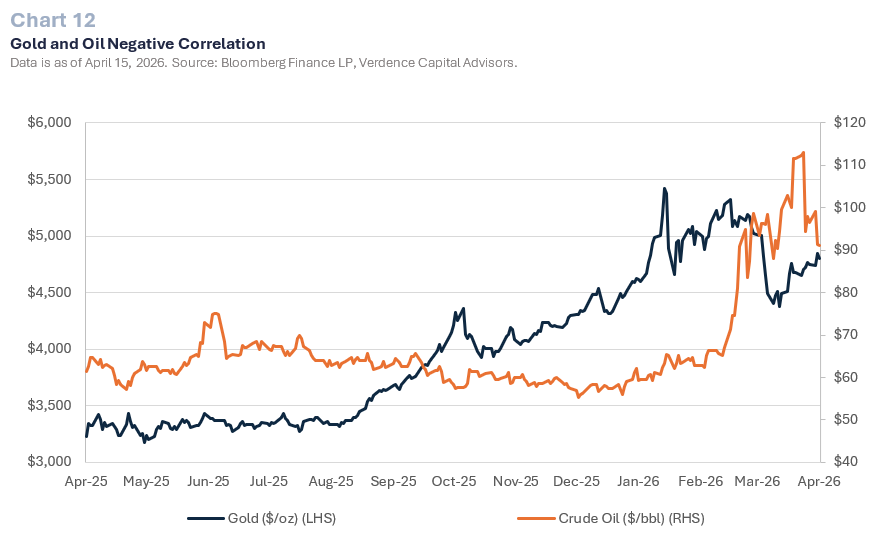

Within the commodity space, we would focus on a broadly diversified approach to commodities for the long run. While gold has been strong over the past year due to a slowing global economy, burgeoning global debt, a weaker dollar, and diversification away from U.S. assets by many global central banks, its safe haven status broke down when the war with Iran started. Instead, gold prices experienced two massive pullbacks in 1Q26 (-14% and -18%) as investors sold many momentum-driven investments. In addition, there has been a strong negative correlation between gold and oil this year, as oil rises gold prices decline. (Chart 12, next page). Given our expectation that oil prices will likely remain higher than we have seen in recent years and likely volatile until the war ends, this could challenge gold prices.

Alternatives Bottom Line:

For qualified investors, we believe the current investing climate is a great opportunity to look for private investments in the real asset space as well as hedge funds that can help mitigate the volatility investors experience in their public market portfolios. Within the public markets, we like commodities as a real asset but are strongly recommending a well diversified approach given the momentum characteristics that some commodities have picked up in recent years (e.g., gold). We would consider focusing on natural resources and infrastructure as a long-term investment.

Real assets can not only perform well in periods of stubborn inflation but also in periods of infrastructure investment.

Verdence View:

Geopolitics is one consideration when we recommend asset allocation. But it is not an overwhelming driver. However, we do realize it can bring a lot of unease for investors, especially given the volatility we have witnessed thus far in 2026. We would prefer to put more weight into the fundamental environment and valuations. From a fundamental perspective, we are constructive about the economy and earnings growth. But we realize there are headwinds in the near term, and current prices have not considered these challenges.

When looking at valuations, investors have quickly forgotten about the war. When looking at price-to-earnings multiples, prices at current levels are not fully reflecting the fact that interest rates may stay higher for longer. We remain constructive long-term, so we will monitor weakness for potential buying opportunities. Especially since history tells us that weakness in midterm election years and in similar geopolitical events often present opportunities for the long run.

As always, if you have any questions about our perspective, please do not hesitate to reach out to your advisor.

Author: Megan Horneman | Chief Investment Officer Past performance is not indicative of future returns

- This is largely attributed to Joe Lavornga, a well known Economist and former White House Advisor.

- https://taxfoundation.org/blog/tax-refunds-one-big-beautiful-bill-act

- “Kevin Warsh’s First Move as Fed Chair Could be a Rate Hike.” Reuters as of March 6, 2026.

- The time period reflects all midterm election years from 1946 to 2022 and the average is a median average.