Private Credit Under Pressure

Speculation has swirled in recent weeks about the private credit market after several publicly traded alternative managers have come under pressure. Blue Owl, a public alternative asset manager had to restrict redemptions from one of its semi liquid credit funds as investors rushed to pull money on default fears. The angst quickly spread to other publicly traded alternative managers (e.g., KKR, Apollo Global Management and Blackstone) as seen by the S&P 500 Asset Management Index down over 15% from its recent peak. In addition, several reputable CEOs and global banks are warning about the default risk in the private credit space (e.g., Jamie Dimon and UBS).

In this publication we want to address the catalysts for the recent anxiety in the public market. We also want to discuss the differences between what is going on in the public markets and what we see in the illiquid private credit markets. Especially our approach to how we evaluate private credit managers.

Catalysts for Recent Sell-off in Public Alternative Managers

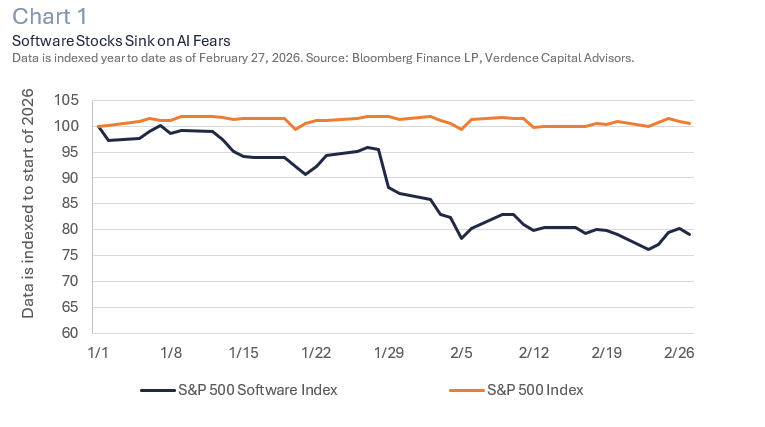

- Default fears: The speculation that AI would reduce the demand for software has caused a broad selloff in software stocks. The S&P 500 Software Index has fallen more than 30% from its recent high (Chart 1). It is estimated that private credit (especially through business development companies) has ~20% of its loans tied up in software companies.1 With the selloff in software stocks, the fears of widespread defaults have increased and spread to other public asset managers that hold these loans.

- Weaker lending standards: During and after the pandemic, lending standards for private credit began to loosen. This is especially true for lower rated companies. For example, we saw a surge in covenant lite structures. These structures allow lenders to reduce or eliminate certain covenants (e.g., cash flow testing, minimum EBITDA levels). We also saw an uptick in pay in kind (PIK) structures which means the borrower can skip interest payments and instead add it to the balance of the loan. This may be tolerable when rates are low, but when it is late in a credit cycle and when the Fed may be on hold instead of cutting rates, these loans can become problematic.

- Refinancing wall: Many loans originated in the aftermath of the pandemic (2020-2021) and this year they are approaching their fifth year. Many loans will need to be refinanced or restructured. It is estimated that between $300-$350 billion of leveraged and private credit is entering a “refinancing window.”

- Liquidity stress: The loans that private credit managers own are not easy to sell quickly. These loans tend to be illiquid and can be longer in duration. When these loans are placed in a vehicle where redemptions are allowed it can create a liquidity squeeze if too many investors want to redeem at the same time.

The Difference Between Public Market Turmoil and Private Market

While we outlined the reasons why investors may be growing nervous about private credit, it is important to understand the difference between what is going on with public asset managers and the truly illiquid private credit space. Those managers that trade publicly and own anything that comes under pressure can easily see their stock price in a downward spiral as investors rush to sell. Especially, if that company is in the business of making loans, fear can turn into indiscriminate selling of other companies in that sector.

That turns into investors rushing to pull money from these companies’ funds, and it creates a liquidity issue and not always because of an underlying credit issue. A lot of recent concerns have been concentrated around business development corporations, illiquid real estate investment trusts and insurance backed vehicles. All of these have the same liquidity challenges when sentiment falls (e.g., redemptions), and some have higher credit risk.

Managers in the illiquid private credit space do not have the same volatility challenges as we have mentioned above. While we acknowledge that some of the above risks may pertain to the illiquid markets (e.g., easing lending standards, AI overspend), private credit as an alternative asset class that has historically proven to be a good long-term investment when the appropriate due diligence is conducted.

How do we Evaluate Private Credit Managers?

Effective due diligence in the illiquid private market starts with deep understanding of the manager’s strategy, risk management, and verifying they have a rigorous underwriting process. That means clarifying what part of the market they target (sponsor vs. non‑sponsor, core direct lending vs. opportunistic/recurring‑revenue risk), how they source and pass on deals, and whether fund size and deployment pace are realistic for those markets and the existing opportunity set. It is important to have in depth knowledge of how private credit managers’ price and structure risk, the amount of leverage they utilize, how tight covenants are, how they evaluate the use of complex features (e.g., pay in kind), what sectors they allocate to and how much concentration they may have.

Equally important is operational, structural and alignment due diligence, given the illiquid and opaque nature of private credit. Understanding the structural matching of liquidity is also a key part of the due diligence process. This is highlighted above with Blue Owl’s struggles where investors no longer have the right to tender a fixed percentage of shares each quarter. Blue Owl’s situation represents a real example of liquidity risk and poor underwriting in semi‑liquid private credit, particularly in concentrated segments like software.

Blue Owl’s situation represents a real example of liquidity risk and poor underwriting in semi-liquid private credit, particularly in concentrated segments like software.

Verdence View

The current struggles in public asset managers are not, in our view, an indication that the private credit asset class is broken. Instead, it reinforces our existing belief that due diligence is extremely important. It’s important in the evaluation of not only private credit, but all alternative managers. In addition, having a knowledgeable team that can evaluate private credit managers to analyze their risk/reward potential for the long run is vital. We believe that private credit will continue to be an important part of a well-diversified alternative portfolio. While we are not adding any additional managers at this time, we continue to favor managers and vehicles with strong underwriting standards, diversified portfolios, and well identified liquidity terms that allow for robust secondary‑market access.

If you have any questions or comments, please reach out to your financial advisor.

Megan Horneman | Chief Investment Officer

Matthew Andrulot | Executive Director of Verdence/RIA+

Past performance is not indicative of future returns