Key Takeaways:

- Light data week contributed to turnaround.

- Recession is still a threat.

- Bond auctions weak; can threaten growth and fuel higher rates.

- Negative seasonality just starting.

- Expect additional downside in the coming months.

Theme of the Week — Too Soon to Say the Bottom Is In?

We welcome last week’s market turnaround however, we do not believe that volatility is behind us and we warn investors of additional downside in the coming months. While some of the sell off that occurred in the beginning of August can be attributed to technicals, algorithmic trading and the unwinding of the Yen carry trade, there are other reasons for the sell off that have not changed. In this commentary, we will identify the factors that we see as additional risk to equities. We will also reiterate that we will look for buying opportunities on the downside but only if prices are discounting risk.

- A light data week for investors: Last week investors did not have much data to absorb. The only major piece of data was the ISM Services Index that came in modestly better than expected. While markets cheered the reading, they also neglected to see the prices paid component jumped which is an inflation concern. While weekly jobless claims did not offer any surprises, continuing claims rose again and are at the highest level since 2021. This week markets will have much more data to digest, including several inflation reports and data on the consumer.

- Recession is still on the table: The economy has not miraculously turned around to support the rebound last week. In fact, the inflation data from the service report should have investors more concerned about the Fed’s flexibility to ease policy. Realistically, the consumer is squeezed and the last domino to fall is the labor market, and that is unraveling. Weekly hours are at the lowest level since April 2020, those working part-time for economic reasons are at a three-year high and temporary workers have been cut for 26 out of the past 28 months. These are leading indicators for higher unemployment.

- Bond auctions an issue: Last week we saw sloppy 10 and 30-year Treasury auctions which sent yields higher. Demand at the 10-year auction was the lowest since December 2022. In the 30-year, primary dealers were stuck buying the most supply since November 2023. Yields will continue to rise if we cannot find buyers for the massive amount of fiscal debt that our country is issuing. This will push lending rates higher for consumers.

- We are in the beginning of negative seasonality: Historically, two of the worst months of the year are August and September. In addition, going back to 1928 there are more pullbacks of 10% or more in the month of October than any other month in the year.

- Capitulation factors not triggered: We look at several indicators (e.g. put/call ratio, VIX, spreads) to decipher if a downturn has reached a level of being washed out. On the final day of the recent weakness (i.e. August 5) not one of capitulation indicators was triggered.

- Earnings will need to come down: With the likelihood of a recession increasing, current estimates for double-digit earnings growth this year and next are unlikely to be achieved.

The Bottom Line

Nothing has changed since the market sell-off in early August. In fact, we see the downside risks for the economy growing, which does not justify equities at current levels. We expect additional downside in the coming months.

Footnotes: Data is as of August 9, 2024.

Source: Bloomberg Finance LP, Verdence Capital Advisors.

Your Economic and Market Detailed Recaps

Key Takeaways:

- Services sector expands by most in four years.

- Consumers slow the pace of spending on credit, but balances still rise.

- Initial claims for unemployment fall by most in a year.

- Global equities post impressive reversal after early week‘s losses.

- Bond yields rise as investors assess the Fed’s path forward.

- Crude oil prices rise on fears of global supply shortage.

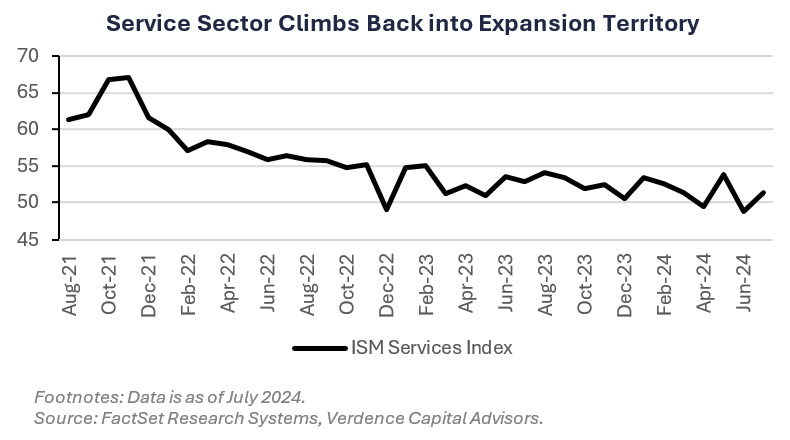

Weekly Economic Recap — Service Sector Climbs Back into Expansion Territory

The U.S. services sector expanded in July by the most in four years according to the ISM Services Index. The employment index increased for the first time since the start of the year and at the fastest pace since September. New orders increased back into expansion territory (a reading above 50).

Consumer borrowing increased by less than expected in June driven by smaller spending on credit-cards. Total credit outstanding increased $8.9 billion, less than consensus estimates for an increase of $10 billion. Revolving credit (i.e., credit cards) declined by the most since 2021.

The US trade deficit narrowed for the first time in three months as the value of exports for goods and services increased by the most since the start of the year. The value of exports increased 1.5%, outpacing the rise in the price of imports of 0.6%. The trade deficit with China increased to a four-month high ($22.3 billion).

Initial claims for unemployment benefits fell last week by the most in roughly a year (17k), falling to 233k. Continuing claims, which run a week behind the headline number, increased to 1.88 million, in line with consensus estimates.

Consumer credit card balances, according to a report by TransUnion, have ballooned to a record $1.14 trillion. The average borrower owes $6,329, an increase of 4.8% YoY. Credit card delinquency rates are higher as well according to the report, as roughly 9% of balances transitioned into delinquency over the past year.

Weekly Market Recap — Global Equities Post Impressive Comeback, but Still Lower for the Week

Equities: The MSCI AC World Index ended the week relatively unchanged as global equity markets staged an impressive turnaround after steep losses ushered in the week. In the U.S., all major averages were lower but clawed back much of their early week losses. In fact, large-cap growth, as tracked by the Russell 1000 Growth Index, ended the week higher for the first time in five weeks.

Fixed Income: The Bloomberg Barclays Aggregate Index was lower for the first time in three weeks. Bond yields moved higher (prices were lower) as investors continued to digest the state of the economy and the Fed’s path forward. High yield corporate bonds and U.S. floating rate instruments were the only areas of fixed income higher for the week.

Commodities/FX: The Bloomberg Commodity Index was higher for the first time in five weeks. Crude oil prices were higher for the first time in five weeks as well as investors weigh the likelihood of a wider conflict in the Middle East that could disrupt global supply. Gold prices were marginally higher for the second straight week.

Data is as of August 9, 2024.

Source: Bloomberg Finance LP, Verdence Capital Advisors.