Key Takeaways:

- Inflationary pressures remain stubborn.

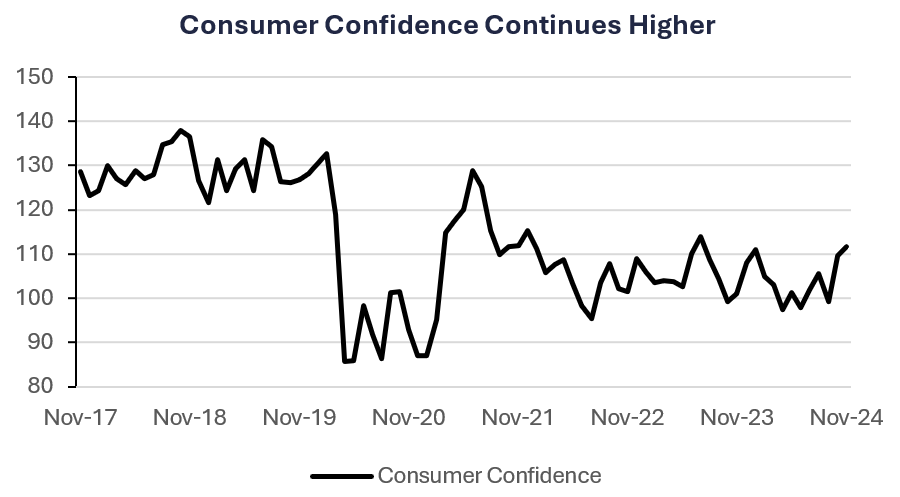

- Consumer confidence climbs on increased optimism for the short-term economic outlook.

- Equity performance broadens after Trump election victory.

- Bond yields volatile, but fixed income posted small gain.

- Gold prices fall by most in over a year on a stronger U.S. Dollar and economic outlook.

Equity Performance Broadens – November Recap

Despite inflation remaning a burden, mixed economic data, and geopolitical strife, global equity markets were positive in November. U.S. equity markets cheered the results from the U.S. election as investors hope for easier regulations and no major changes to taxes. U.S. bonds as measured by the Bloomberg Aggregate Index were positive as well but it was not an easy ride. Yields were volatile as investors weighed the risk of inflation on Trump’s campaign promises but also a softer economic picture in the U.S. In this weekly insights, we provide a recap of November from an asset class and economic perspective..

- Inflation Remains Stubborn: Headline inflation as tracked by the Consumer Price Index increased at its fastest annualized pace in three months (2.6%). The Fed’s preferred inflation gauge, PCE Core, also increased (2.8%) to its highest-level annual change since April.

- Fed Continues to Ease: The Federal Reserve cut interest rates by 25bps to a range of 4.50% – 4.75%. However, the minutes indicated the need for “gradual” moves in rates in the future.

- Consumer confidence improves but spending slows: Consumer confidence, as tracked by both the University of Michigan and the Conference Board, moved higher on the back of increased optimism for the short term. However, retail sales at the core level (excluding building materials, gas, food and autos) declined for the second time in three months.

- Mixed housing data: Confidence among homebuilders increased to a seven-month high and sales of previously owned homes increased amid a sharp drop in mortgage rates. However, new home sales fell to the lowest level in two years.

Global Equities – Rally Broadens: The MSCI AC World Index was higher for the sixth time in seven months. U.S. markets led the rally as performance broadened.

- U.S. large cap rally broadens: The S&P 500 finished the month at a record high and posted its best monthly performance of the year. All 11 sectors rallied but it was led by financials and consumer discretionary stocks. Healthcare and materials lagged.

- Small caps lead U.S. gains: The Russell 2000 Index posted its best return this year on optimism about Trump’s campaign promises.

Fixed Income – Yield volatility: The Bloomberg Aggregate Index was higher in November, but it was a volatile month. The 10YR Treasury yield reached its highest level since July on the risk of inflation.

- Gains led by credit: Credit outperformed Treasuries in November. Investment grade bonds, municipals, high yield and emerging market debt all rallied.

Commodities: The Bloomberg Commodity Index finished the month marginally higher. The gains were mixed as energy and soft commodities were the only positive sectors for the month.

- Gold prices falter: Gold prices posted the worst month since September 2023. Gold prices have been under pressure as the U.S. dollar rallies on Trump’s win.

- Energy led by natural gas: Energy posted a gain, but it was primarily led by gains in natural gas as oil prices declined for the month.

Your Economic and Market Detailed Recaps

- Consumer confidence climbs to highest since July 2023.

- Services inflation remains stubborn.

- Fed officials see “gradual” interest rate cuts in the future.

- S. equities carry global performance.

- Treasury yields fall as investors weigh economic data.

- Commodities lower driven by crude oil.

Weekly Economic Recap — Inflation Remains Sticky, but Confidence Higher

Home prices, as tracked by the S&P CoreLogic Index, increased broadly in August. The gauge of 20-cities increased 4.6% year over year compared with the previous month’s increase of 5.2% year over year. Cleveland and Phoenix led the gains for the month.

New home sales fell to the lowest level in nearly two years amid hurricane disruptions in the South. Sales in the South fell to an annualized rate of 339K, the slowest pace since April 2020. Supply of new homes has risen to levels last seen during the Great Recession, pushing the monthly inventory to 9.5 months, the highest in two years.

Consumer confidence as measured by the Conference Board, increased to its highest level since July 2023. The present conditions index increased to an eight-month high, while the expectations index (next six-months) increased to a near three-year high.

The Fed’s preferred inflation gauge, PCE Core, increased in October and pushed the year over year growth rate higher (from 2.7% to 2.8% YoY). Services inflation increased at the fastet annual pace since May (+3.9%). Higher stock prices drove portfolio management services higher, increasing the most on an annualized basis since November 2021.

The Federal Reserve November meeting minutes indicated officials’ support for a careful approach to future interest rate cuts. The minutes indicated, “if data came in about as expected… it would be appropriate to move gradually toward a more neutral stance.”

US economic activity expanded at a robust pace in 3Q24, according to the second reading of GDP data. Consumer spending, which accounts for ~68% of the headline number, increased at its fastest pace this year (3.5%).

Weekly Market Recap — U.S. Equities Lead Global Rally as Treasury Yields Slide

Equities: The MSCI AC World Index was higher for the second straight week. U.S. markets led global equity performance despite a shortened Thanksgiving trading week. The Dow Jones Industrial Average and S&P 500 both finished the week at record highs. Technology stocks, specifically semiconductors, were higher after the Biden administration announced additional barriers to sales of equipment to China that were not as aggressive as previously anticipated.

Fixed Income: The Bloomberg Aggregate Index was higher for the second straight week and by the most since August. Treasury yields finished the week at their lowest levels since October despite stubborn inflation. All fixed income sectors were higher for the week with relative outperformance seen from investment grade corporate bonds.

Commodities/FX: The Bloomberg Commodity Index was lower for the second time in three weeks. Crude oil prices were lower for the second time in three weeks as global supply risks eased. Gold prices rallied for the week as the U.S. dollar dropped. Grains prices were lower, specifically wheat, on increased supply from Russia.

Data is as of November 2024.

Source: FactSet Research Systems, Verdence Capital Advisors