Can AI Give You Investment Advice? What Investors Need to Know

The use of artificial intelligence through large language models (LLMs) such as ChatGPT, Gemini, and Claude are quickly being integrated into everyday life. ChatGPT, Gemini, and Claude together count nearly 2.5 billion active users. This is up from ~1.5 billion in 2025.1 Users are finding recipes, planning travel, summarizing data, formulating emails, and doing research. However, we are also witnessing a growing trend of investors using LLMs to assist with basic financial tasks (e.g., budgeting, taxes). This is in addition to picking stocks, creating asset allocation models and analysis of current investment allocations.

In this quarterly white paper, we want to help investors understand how LLMs actually work. We also want to show where they can be useful, and where they fall short, particularly when it comes to investment decisions. Our goal is not to discourage the use of new technology. It is to give investors a clearer picture of what these tools can and cannot do. We explain why we believe constructing and managing a long-term asset allocation requires human expertise, client knowledge, and ongoing accountability.

How Do Large Language Models Actually Work?

At their core, LLMs are exactly what their name suggests, a model that is built to work with language, not numbers. To understand where they belong in investment decisions, it helps to start with what these tools do. A large language model is a text predictor. The model trains on vast amounts of writing from books, articles, websites, blogs and online forums. From that material, it learns the patterns of how words tend to follow other words across different contexts.

When you ask an LLM a question, it is not thinking, calculating, or looking up facts. It is choosing the most likely next words based on what it has seen before. The response sounds like a thoughtful answer because the model has learned what thoughtful investment advice sounds like. This is not because it has any of its own. Building a long-term asset allocation model is a math problem. An LLM is not built to solve math problems, only to produce language that sounds like the answer to one.

Can AI Build an Optimized Investment Portfolio?

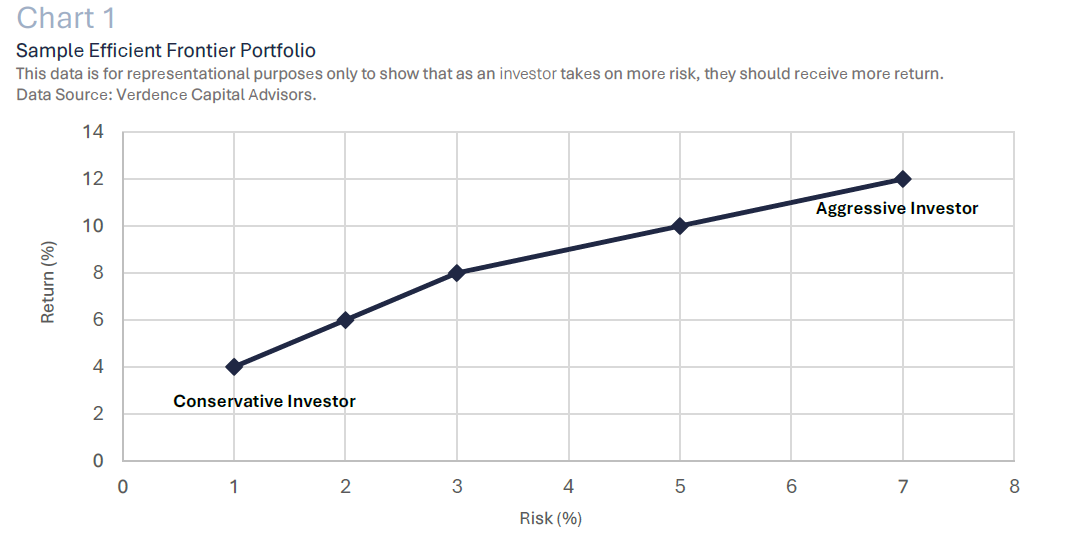

The difference between language and math becomes clear when you look at how a real investment portfolio is built. When investors and advisors talk about portfolio optimization they are usually referring to mean-variance optimization. Harry Markowitz developed this mathematical method by in the 1950s, earning him a Nobel Prize. Professional portfolio construction still rests on it today.

The method takes three inputs: expected returns, expected volatility, and how correlated the investments are expected to be in the future. From those inputs, it produces a range of portfolios that aim to deliver the best possible return for a given level of risk. This is known as the efficient frontier (Chart 1). Then a Financial Advisor selects the portfolio on that range that best fits the investor’s long-term goals, time horizon, and ability to tolerate losses. The result is an allocation built on math and shaped by judgment about the investor. An LLM cannot generate the inputs the math requires, it does not run the calculation and cannot make the judgment that has to follow.

How Current Is the Data Behind AI Investment Tools?

Even setting aside the math problem, there is a second limitation when using an LLM for portfolio advice. The model is always working from yesterday’s information. Each LLM has a training cutoff date (Table 1), which is the date after which it has seen no new information. Interest rate changes, earnings results, geopolitical events, and shifts in valuations that occurred after that date are all unknown to the model.

When an investor asks an LLM for an investment recommendation today, the answer may be based on a view of the world that is six months, a year, or several years out of date. The model does not bridge that gap, and it answers with the same confidence whether the data behind it is current or stale.

That matters for long-term asset allocation in two ways. First, any investment decision should start with where markets are right now, and the LLM may not know that. Second, the assumptions baked into the model’s training may no longer hold. For example, what bonds were expected to do, how different investments tended to move together, what valuations once looked reasonable can shift quickly in ways the model has not seen. The output is current, but the thinking is not. The model writes every response with the same confidence, and investors have no way to tell the difference.

Is Pasting Your Portfolio Into an AI Tool a Good Idea?

One trend we have seen is investors using LLMs as a second opinion on their current portfolio. This is often done by pasting their current holdings into the LLM and asking the model to evaluate it. We realize that it could make sense if the model has access to the actual holdings, the feedback should be more useful.

Unfortunately, giving the model more data does not change what the model is. It is still not performing real optimization. Its information may still be out of date and the response still reads like a real analysis while no real analysis has been done.

The model still cannot see everything that truly shapes a good investment allocation. It does not know the investor’s tax situation, liquidity needs, whether they have concentrated stock positions, or how that investor tends to behave when markets fall. The output may look like a thoughtful second opinion, but it is built on the same limitations explained earlier.

There is also a practical concern worth monitoring. When investors paste portfolio details and personal information into an LLM, a third-party server may store that information. They may also retain it, use it for training, or it may be exposed in a security breach.

Where Does AI Get Its Investment Information?

LLMs train on internet content, and most of the investment content online is written for retail audiences. This includes trading forums, personal finance blogs, marketing material, and outdated articles. Peer-reviewed academic finance, institutional research, and the work that professional investors rely on makes up a much smaller share of what the model has seen. A lot of that work sits behind subscriptions, including Bloomberg, FactSet, and Morningstar Direct.

To the model, a Reddit thread and a peer-reviewed paper are both just text, and they sit in the training data at roughly the same weight. A useful reminder of how retail investors can move markets came in January 2021. A coordinated effort on Reddit’s WallStreetBets forum sent GameStop’s share price up more than 1,600% in a matter of weeks. The stock then collapsed and many investors who bought late sustained significant losses. So when an investor asks it about portfolio construction, it’s also pulling the posts, the hype and the rationalizations from that period all in the same training data.

The risk grows when you consider how investors use these tools. Most ask follow-up questions until the model agrees with them. Remember, the model is built to be helpful and agreeable. What you end up with is confirmation bias dressed up as investment advice, an answer that feels validated when the user has talked the model into it.

What you end up with is confirmation bias dressed up as investment advice.

Hallucinations and the Herd

Another limitation worth noting is that LLMs can produce what the industry calls hallucinations. These are confident, specific-sounding answers that are simply wrong. This may include made-up fund symbols, expense ratios that are inaccurate and historical returns that were not real. An LLM model delivers all of it with the same confidence as real information making the errors difficult for an everyday user to spot.

Now consider that millions of investors are asking the same handful of models the same kinds of questions and acting on similar answers. We have seen herd behavior move markets before without any help from AI. Add a tool that pushes flawed analysis out to everyone at once and you have a recipe for amplified volatility in markets that are already prone to it.

LLMs Do Not Know You

Know Your Client is a foundational principle of investment advising. It is a regulatory requirement and the starting point for any portfolio decision that has a chance of being right for a client. An LLM model does not know an investor, it only knows what was typed in the chat box that day. And that is rarely the full picture.

Real portfolio management is also an ongoing job, not a one-time recommendation. A real advisor is monitoring the portfolio over time and deciding when to rebalance. They also are looking for opportunities to harvest tax losses and coordinating with the investor’s CPA and estate attorney. An LLM produces an answer in a single moment and then forgets that the conversation happened.

Perhaps most importantly, an LLM is not a registered investment advisor. It is not regulated and it has no fiduciary duty to act in your best interest. A professional advisor does, and that obligation shapes every recommendation.

What is an AI hallucination? When an AI system produces information that sounds confident and plausible but is wrong or made up.

How Verdence Uses AI

It may be easy to read this white paper as a broad criticism of artificial intelligence. That is not our view. AI plays a meaningful role in the work we do. We believe it will continue driving efficiency in ways that translate into a better experience for our clients. The question is not whether to use it, but where does it add value and where does it not belong?

How Does AI Help Investment Advisors Work Better?

From an investment strategy perspective, LLMs help our team move faster through research. It’s much easier to pull insights from large data sets in less time than before. It can summarize dense regulatory filings, earnings reports, and other long documents. This in turn lets us spend more time thinking and less time reading. LLMs do not form our views or draw conclusions, but they help organize thoughts and surface questions worth asking. The arguments, the house view, and the final positions are our own.

In our work with clients, AI helps us prepare for meetings by organizing notes and gathering relevant context we might otherwise miss. It is useful for stress-testing scenarios and modeling outcomes we want to walk through together. It can also support routine operational tasks that allow our team to focus more of their time on the work that matters.

Where Does AI Fall Short in Portfolio Management?

What we do not use AI for is just as important. We do not use it to build long-term asset allocations. We also do not generate investment recommendations, or replace the judgment that sits behind every decision we make for our clients. That work continues to require human expertise, real knowledge of the client, and the ongoing accountability that defines a fiduciary relationship.

This is what we believe is the right use of this growing technology. AI belongs as a tool that supports work, not one that replaces the judgment and the relationships behind it.

AI belongs where it organizes thinking, summarizes dense material, and surfaces questions worth asking, but the judgment, conclusions, and final positions stay human.

Verdence View

Artificial intelligence is here to stay, and its capabilities continue to grow. For investors, the right response is not to avoid it, but to understand it. LLMs are remarkable tools for many tasks, but they are not built for the work of constructing a long-term investment plan. They cannot perform the math and do not have current market information. They also do not know the investor and carry no responsibility for the outcome of any recommendation they produce.

A better question to ask is not whether AI should be involved in investment decisions, but how? AI can help advisors work faster, dig deeper, and spend more time on the parts of the job that genuinely require human judgment. That is where we believe it belongs, and that is how we use it at Verdence.

If you have questions about how we use technology in our work, or how we think about your portfolio, please reach out to your advisor.

If you have questions about how we use technology in our work, or how we think about your portfolio, please reach out to your financial advisor.

Megan Horneman | Chief Investment Officer

Past performance is not indicative of future returns