Investors looked beyond a slowing economic backdrop, stubborn inflation pressures and ongoing tariff uncertainty in 3Q25. Instead, the resumption of interest rate cuts by the Federal Reserve boosted stocks, bonds and commodities. Although the quarter had a choppy start, global equities (i.e., MSCI AC World Index) came to end the quarter at a record high (Chart 1). That was after the Fed suggested more rate cuts were ahead, trade negotiations started, corporate earnings were stronger than expected and momentum continued to build around artificial intelligence stocks.

Bonds broadly gained as investors priced in more rate cuts despite inflation moving higher. The Bloomberg Commodity Index erased the losses seen in 2Q25, but it was primarily driven by gold, making more than 10 fresh new record highs during the quarter. Even the U.S. Dollar which had been off to its worst start to a new year since 1986 (through 2Q25) rebounded to end the quarter moderately positive.

LISTEN NOW: Alternate View Podcast

As we navigate through the remainder of 2025, the equity market that is repeatedly making record highs is concerning. Especially as economic growth is decelerating and the Fed may not be as flexible as investors are expecting. In this quarterly review and Q4 2025 market outlook, we will discuss the growth trajectory of the economy. We will also highlight our recommendations for each asset class and how we expect the investment landscape to evolve over the coming months.

U.S. Economy – Slippery Slope

The U.S. economy is defying most expectations this year as the tariff implications have been muted. Also due to capex spending surging due to the evolution of AI, and the consumer continues to spend despite stagnated real wage growth (Chart 2). The tariff distortions that drove 1Q25 GDP into negative territory have reversed. According to the Atlanta Fed GDPNow model, the economy is expected to have grown 3.8% for the second consecutive quarter in 3Q25.1 If this comes to fruition, it would be the best two quarters for GDP since 3Q/4Q23.

In the near term, we see downside risks to the economy and are concerned that stubborn inflation is being disregarded by many Fed officials. We admit the consumer has been stronger than we anticipated. But we view consumer spending on a slippery slope. Especially since the labor market is clearly weakening and inflation is continuing to compound. Plus credit card delinquencies are high, and household savings rates are below average.

In addition, we are witnessing consumer confidence softening at nearly all income levels. This is in addition to key age demographics for spending (ages 35-54). In fact, in the most recent University of Michigan Consumer Confidence Survey, consumers have the worst outlook for their finances over the next five years on record (records began 2011) (Chart 3). When you combine the growing nervousness of consumers with the less favorable job prospects, this is a risk to spending. Eventually, the consumer will reach a breaking point and pull back on spending which can have a direct impact on GDP.

LISTEN NOW: Markets With Megan Podcast

Despite the Fed cutting interest rates, inflation is a persistent problem. This adds a layer of risk to economic growth. Especially, if the Fed continues the rate cuts that the market is pricing in (i.e., two more in 2025, four to five in 2026).2 We realize that inflation has improved substantially from the pandemic related pricing pressures (e.g., supply chain, Government stimulus). However, the recent trajectory has been in the opposite direction of the Fed’s target (Chart 4).

When we focus on service-related prices, the inflation story is worth watching. This is especially since most of Americans’ spending is in the service sector. According to the Consumer Price Index, the growth in service prices (excluding energy) has decelerated from the peak in the aftermath of the pandemic. But prices are growing well above the historical average seen prior to the pandemic (Chart 5). Remember that inflation compounds, so even though the pace of growth is slower, year after year of compounding price increases negatively impacts consumers.

Inflation and the Fed: How much can the Fed cut rates?

There has been great debate about the timing and magnitude of interest rate cuts in 2025. Inflation is not expected to reach the Fed’s target rate until 2027. And the progress on its downward trajectory is slowing. Therefore the Fed has maintained a “wait and see” approach to interest rate policy.

Inflation has improved substantially since its peak after the pandemic. But the growth in core inflation (on an annual basis) has been above 2.5% each month this year. In fact, for the past two consecutive months (May and April), the annual growth rate of PCE core has accelerated. (Chart 5).

This lack of progress may be reflecting the first wave of tariffs (10% baseline). But the frameworks approved ahead of the August 1st deadline and any reciprocal tariffs imposed after the deadline may not be reflected in data until 4Q25. In addition, the components of inflation that the Fed considered “sticky” are still well above levels the Fed would feel comfortable with easing policy.

As a result, we expect the Fed to err on the side of caution. We do expect the Fed to continue easing monetary policy but the magnitude of rate cuts that are currently priced into futures markets (4-5 rate cuts by the middle of 2026) may be too optimistic. We expect one rate hike in 2H25 (likely December) and the Fed to deliver another commitment to waiting to see how the tariffs impact inflation and the labor market.

While economic data has been disrupted by the Government shutdown, some of the non-government surveys we have received suggest pricing pressures remain a concern. In the most recent New York Fed Consumer Expectations Survey, the expectation of inflation over the next year has been moving away from the Fed’s 2% target (Chart 6).

Impact of Tariffs

We also need to remember that we do not yet know the full impact from tariffs. What we have seen is that companies are absorbing some of the tariffs. But the inflation data acts on a lag, and the Government shutdown further disrupts the data. The Fed is opting to focus more on the softer labor picture, but we are cautious that they may not have the flexibility that investors are expecting.

While we are cautious in the near term, we remain optimistic about future growth prospects. In 2026, the economy gets a boost from a favorable tax package. This can help to offset some of the tariff related pricing pressures. We also expect the solid contribution to growth from capex spending on AI related infrastructure to continue.

The U.S. economy has defied most expectations this year…

we remain cautious in the near term, but optimistic about the future.

Global Equities – Brace Yourself for a Rocky Road

The MSCI AC World Index ended 3Q25 at a record high. And it has continued its upward trajectory as we move through the end of what has been an impressive year. Better than expected earnings and the Fed cutting interest rates has supported the rally. But we are concerned that there are not many upside catalysts in the near term.

Instead, we see that complacency is emerging around the AI capex surge. Plus credit risks are underpriced, the bar for economic and earnings growth is high, and inflation is being ignored. These factors are likely to cause market swings that may disrupt the ongoing optimism. And this disappointment can lead to market weakness.

As a result, in an environment where markets are making record high after record high it is important to remain disciplined. Unfortunately, valuations (price to earnings multiples) for many global indices are trading at levels that we see as overpriced. And they are not rewarding investors for the potential downside risks to the overly optimistic attitude in the market (Chart 7). Therefore, we recommend the following as we close out 2025.

Be careful chasing momentum:

It is easy to fall into the fear of missing out mentality. That’s especially true when watching select areas of the global stock market (e.g. U.S. Large Cap growth/technology) repeatedly hit fresh record highs. We are enthusiastic about the evolution of AI but realize that select sectors and stocks are exhibiting “bubble like characteristics.” This leaves room for disappointment and these sectors susceptible to large market swings.

As a result, we recommend being underweight growth stocks/sectors in our global asset allocation compared to the benchmark. We also believe that if you are highly exposed to these growth sectors, it is time to trim this exposure. Valuation corrections are extremely hard to predict and can be painful. We have seen that while markets can ride high on momentum, they can also overshoot in a downturn.

Small and midcap a better opportunity than large cap:

Small and midcap stocks can be highly economically sensitive and struggle in times of an economic downturn. Given our expectation of slower economic growth in the near term, recommending these equities may seem counterintuitive. However, small and midcap stocks at current levels may be reflecting the downside risk to growth much more than their large cap counterpart.

In addition, while we may not be as optimistic about the flexibility the Fed has (especially into 2026) as the futures market, any move lower in rates should help small and midcap stocks. If your allocation is concentrated in U.S. large cap, we believe it is time to diversify into other U.S. market cap areas.

Be diversified globally:

In the near term, valuations seem stretched in international markets, like U.S. markets. However, over the long term we believe there is still room to catch up to U.S. equities (Chart 8). In addition, international developed equities are not as concentrated in tech names, which could smooth out returns in times of valuation corrections in expensive U.S. sectors.

Rebalance where necessary:

This year’s impressive rally across many global indices has driven significant gains in select investments. As a result, some investors may now be overweight certain assets relative to their strategic or tactical recommendations. It is prudent to revisit your asset allocation. This is to be sure that you are aligned with your long-term goals. In some instances, profit taking may be necessary, especially with our expectation that volatility is likely to accelerate into year end.

We are optimistic about global equities in the long run but are selective in the near term. This is given the elevated valuations across many areas of the global equity market. U.S. large cap equities may be fully reflecting the expected economic and earnings growth from AI, the favorable tax package in 2026 and muted impact from tariffs. Therefore, we are underweight U.S. large cap equities across all our investment models (compared to the benchmark). Within U.S. equities, we are overweight value vs. growth. This is due to better relative valuations. In addition, we would favor small and midcap equities over large cap equities given more favorable valuations. Internationally, we favor developed international equities over emerging market equities.

We are optimistic about global equities in the long run but are selective in the near term.

Fixed Income – Focus on Diversification and Quality

The resumption of Fed rate cuts and expectation of more to come has boosted fixed income in 2025. This is despite stubborn inflationary pressures and the uncertainty around what tariffs may do to future inflation.

With bonds (as measured by the Bloomberg Aggregate Index) off to the best start to a year since the pandemic (2020)3, we reiterate our defensive positioning from a duration and credit quality perspective. We remain concerned about the long-term structural risks associated with a burgeoning trade deficit, slower demand and uncertain inflation outlook. We would generally recommend the following for fixed income investors.

Duration is important:

Long term interest rates are much more sensitive to expectations for the deficit and inflation. We expect both factors to negatively impact long-term bonds. As a result, we believe that investors should focus on intermediate maturing bonds as portfolio diversifiers. Intermediate bonds can help mitigate interest rate risk and offer price return potential as the Fed cuts rates and the economy slows.

Avoid credit:

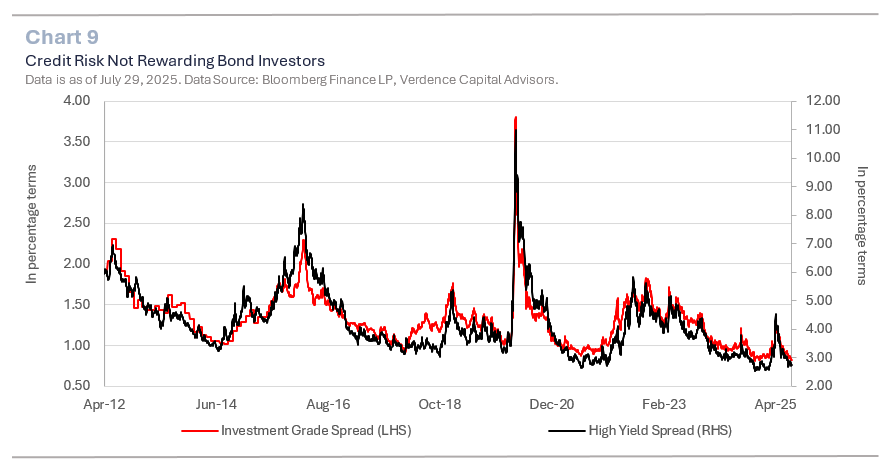

Corporate bonds (both high yield and investment grade) are not rewarding investors for the risk. The extra yield that investors demand from corporate bonds over the safety of a Treasury bond is hovering near historically low levels. Instead of riskier bonds, investors should consider focusing on quality over yield (Chart 9).

Bonds should serve as a portfolio diversifier, but investors should be aware that selected fixed income sectors are overpriced (e.g., credit). Long term fixed income returns may be hampered by supply and inflation volatility. Instead, investors should be patient and look for opportunities in intermediate maturing bonds and focus on quality over yield.

Alternatives – A Shelter from Expensive Public Market

For qualified investors, alternative investments can perform well in periods of stretched public market valuations and slowing economic growth. On the private side, managers have more flexibility and time to be able to find and make good long-term investments. For qualified clients that invest in private investments, they are spared the daily volatility seen in public markets. And historically they have been offered an uncorrelated asset with robust risk adjusted return opportunities.

Not only are alternatives good for an added layer of asset class diversification but from a vintage year perspective, it is important to have some diversification. Historically, periods of economic weakness have offered private equity managers the opportunity to find attractive long-term investments. We like private credit but would not add to it at this time. This is because the space is getting crowded and risks are rising. Due diligence is critical in all private investments but especially in private credit.

Real Estate

We believe that one of the more attractive long-term areas of alternatives is in the real asset space. Real assets can not only perform well in periods of stubborn inflation but also in periods of infrastructure investment. The infrastructure investment that is occurring due to artificial intelligence (e.g. electricity) and the potential for price appreciation and income should benefit investments in the real asset space. But diversification and active management is important in a period of slowing economic growth.

Gold

Gold prices have been supported by many different factors in 2025. This is including trade uncertainty, a slowing global economy, burgeoning global debt, geopolitical tensions, a weaker dollar, and diversification away from U.S. assets by many global central banks. According to the World Gold Council, total gold demand rose 45% year over year (as of 2Q25) and is expected to be strong for the foreseeable future.

We believe gold has diversification benefits in a portfolio. But investors should be wary of the extreme overbought conditions with gold prices at record highs. In fact, the Relative Strength Index for gold prices rose to 87 recently. This indicator has only been above current levels, less than 0.07% of the time over the past 50 years. (Chart 10). When investing in commodities as a portion of real asset exposure, we would focus on a diversified portfolio of a variety of different commodities. This should help smooth out returns over the long run from select commodities that may be subject to volatility but also add the diversification benefit of holding real assets.

Alternative investments can perform well in periods of stretched public market valuations and slowing economic growth.

The Bottom Line

We are concerned that investors may be becoming complacent on how easy investing is after the second consecutive year when all three major asset classes (i.e. global stocks, bonds and commodities) are on pace to rally. We are in a highly uncertain economic, political and inflationary environment that is getting overshadowed by the euphoria that is surging over the future of AI and the benefits to the global economy. There is no doubt that AI is a revolutionary technology that can have many added benefits for businesses and consumers. However, we have seen revolutionary technology before, and we have seen how that can turn from optimism to euphoria quickly and then eventually collapse into reality.

We remain optimistic about the long run of what AI can do for our economy so we will continue to look at periods of weakness as potential buying opportunities. However, we will remain disciplined about paying the appropriate price for an investment. Our asset allocation will reflect the outlook for the economy, interest rates, inflation and earnings growth as opposed to euphoria over one innovation.

As always, if you have any questions about our perspective, please do not hesitate to reach out to your advisor.

Author: Megan Horneman | Chief Investment Officer Past performance is not indicative of future returns

1: Atlanta Fed GDPNow estimate as of October 15,2025

2: Futures market pricing is as of October 20, 2025

3: As of September 30, 2025.